Can You Keep Your HDB and Buy an EC? Here’s the Truth

It’s a common scenario: your HDB has reached its MOP milestone, you’re in a comfortable financial position, and you’re tempted by the idea of upgrading—but without letting go of your current flat. The thought of moving from HDB to EC while holding on to your existing property is appealing. More space, better facilities, and possibly an investment property on the side.

But is it really possible?

Let’s break down the rules, the costs, and the strategies so you know exactly what’s allowed—and what’s not.

Understanding the Rules

HDB has strict policies when it comes to owning multiple properties. The key principle is that you can’t own an HDB flat and buy a new EC directly from a developer at the same time.

If you want to purchase a new EC, you’ll need to sell your HDB within six months of getting the keys to your EC.

However, the situation changes if you’re buying a resale EC that has crossed its own MOP (five years from TOP). Resale ECs are treated like private property, meaning you technically can keep your HDB.

But Here’s the Catch — The ABSD

If you buy a resale EC while keeping your HDB, you’ll face the Additional Buyer’s Stamp Duty (ABSD), which is:

20% of the purchase price for Singapore Citizens (second property rate)

30% for Permanent Residents

This means you’ll need substantial cash or CPF savings to cover the upfront costs—on top of the usual down payment, legal fees, and renovations. On a $1 million resale EC, that’s $200,000 in ABSD for a Singapore Citizen—payable upfront in cash or CPF. You can apply for an ABSD remission if you sell your HDB within a strict timeline, but that defeats the purpose of keeping both properties.

Financing Hurdles You Can’t Ignore

Even if ABSD isn’t a dealbreaker, financing might be. The Total Debt Servicing Ratio (TDSR) limits your total monthly debt repayments (including car loans, credit cards, and housing loans) to 55% of your gross monthly income.

Example:

Monthly income: $12,000

55% TDSR limit: $6,600/month for all debts combined

If you still have a loan on your HDB, your allowable loan amount for the EC could be significantly reduced. This means you’d either need to:

1. Use a large cash/CPF down payment, or

2. Settle your HDB loan first.

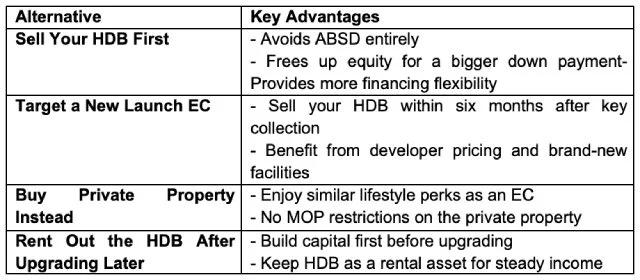

Strategic Alternatives

If your heart is set on an EC lifestyle but you don’t want to part with your HDB, you have a few potential workarounds:

The Reality Check

Holding on to two properties can sound glamorous, but the numbers don’t lie. Between ABSD, financing limits, and ongoing maintenance costs, it’s a move that works for only a small percentage of owners.

That’s why most people who make the shift from HDB to EC do so by selling first. It frees up equity, avoids stamp duty, and simplifies the buying process.

Why a Property Agent Matters Here

This is one of those decisions where having a knowledgeable property agent in Singapore is invaluable. A good agent can:

Assess your eligibility and financial readiness

Advise on the timing of your sale and purchase to minimise disruption

Help you shortlist EC options that suit your budget and goals

With the right guidance, you can make a move that enhances both your lifestyle and your long-term financial health.

Bottom Line

Yes, you can keep your HDB and buy an EC. But for most, it’s not the most practical or cost-effective choice. If your goal is to upgrade while building wealth, selling your HDB first often delivers better returns and fewer headaches.

If you’re ready to explore your best move—whether upgrading, investing, or restructuring your property portfolio—connect with NeezaNizam. We can help you weigh your options with clarity, crunch the numbers, and make a confident decision for your next property chapter.